Can you imagine getting $500 less in your mailbox each month starting in 2032? That’s due to planned Social Security benefit cuts. These aren’t opinions but what the figures show.

No warning. No gradual phase-out. Just a sudden 24% slice off your monthly check. For a lot of retired Americans, that would mean choosing between groceries and medicine. With budgets already tight between utility bills and rent, this would be tough for many. And no, it’s not some scary prediction but the current reality. And the hard truth is, no matter which state you live in, you could feel the impact.

This blog explains everything you need to know. To stay informed and know your options today, we need to understand the issue clearly. This isn’t about politics; it’s about facing facts and acting now.

What are the Social Security benefit cuts for 2032

Let’s start at the beginning because this stuff can be confusing, but it’s simpler than you think. Every time you get paid, a bit of your earnings goes towards Social Security. Here’s the thing – that money doesn’t sit in some account just for you. It gets used right away to pay the people who are retired today. Today’s workers fund today’s retirees. That is how the system was designed.

But here is the thing. The system also has a backup savings account called the trust fund. For many years, Social Security was bringing in more money than it was paying out. The extra went into that trust fund as a cushion.

The retirement cushion is shrinking fast. More folks are retiring than ever, yet the payroll tax cash coming in isn’t covering the benefits going out. So the program has been quietly dipping into its trust fund reserves every single month to make up the difference.

According to the Social Security Administration, reserve funds will be depleted by 2032, which is less than seven years away.

What does “insolvency” actually mean for you? It does NOT mean Social Security disappears. It means the savings account hits zero. After that, the program can only pay out what it collects in monthly payroll taxes. And that amount is only enough to cover about 76 to 77 cents of every dollar owed. The law then automatically triggers a cut of around 24%, for every single beneficiary, in every single state.

How Did We Get Here? The Background of This Crisis

Social Security has been around for more than 90 years. And for most of that time, it worked pretty well. There were plenty of working-age Americans paying into the system and a smaller group of retirees collecting from it.

Then something shifted.

In the late 2000s and early 2010s, baby boomers, those born between 1946 and 1964, began retiring in huge numbers, making the Social Security system much more expensive. Their mass exit continued to increase over time, really shifting the money aspects of Social Security.

Consider this: when Social Security first began, it had about 40 workers supporting each retiree. Now, only around three workers support one retiree. There just aren’t as many people contributing today. More people are collecting. That gap has to come from somewhere.

On top of that, people are simply living longer. Someone retiring at 65 today might collect benefits for 25 or even 30 years. That is a lot more money going out than the original planners ever expected.

The Social Security Trustees have warned about this for years. In their 2025 report, they predicted the trust fund would run out in 2033. The situation got worse, though; recent changes pushed the deadline up by a year to the end of 2032. This happened due to new ways of taxing retirement benefits in federal laws..

Here is another important fact: for 16 straight years, Social Security has been spending more than it earns. Every year, it dips deeper into those reserve savings. And those savings are nearly exhausted.

The $500 Monthly Cut, What the Numbers Really Mean for Everyday Life

Here is the number that made headlines when the latest report came out.

If the trust fund runs dry in 2032 with no changes made, the average monthly Social Security benefit would be cut by roughly $500 per month. That is what the Social Security benefit cuts 2032 projection actually translates to in real dollars.

That is a 24% reduction. Across the board. For everyone.

Key Numbers at a Glance

| Fact | Figure |

| Projected trust fund depletion | End of 2032 |

| Automatic benefit cut at insolvency | 24% |

| Average monthly cut (national) | $500 |

| Total Americans affected | 63 million |

| Share of US population affected | 1 in 5 Americans |

Source: Committee for a Responsible Federal Budget & Social Security Administration, June 2026

Now, $500 a month may sound abstract, so let’s break it down.

The Bureau of Labor Statistics’ 2024 Consumer Expenditure Survey says the average retired household spends around $438 monthly on groceries. That figure is about $461 when adjusted for inflation in 2026.

This $500 monthly Social Security decrease is more than what many seniors spend on food at home in a month.

Imagine being on a fixed income and facing this cut – you’d likely need to drop a prescription to make ends meet.

Skipping a doctor visit. Turning the heat down in winter. For retirees who live close to the edge, this is not an inconvenience. It is a crisis.

And lower-income retirees feel it the hardest. They have fewer savings. No investment accounts to fall back on. For many of them, Social Security is not extra money; it is the only money.

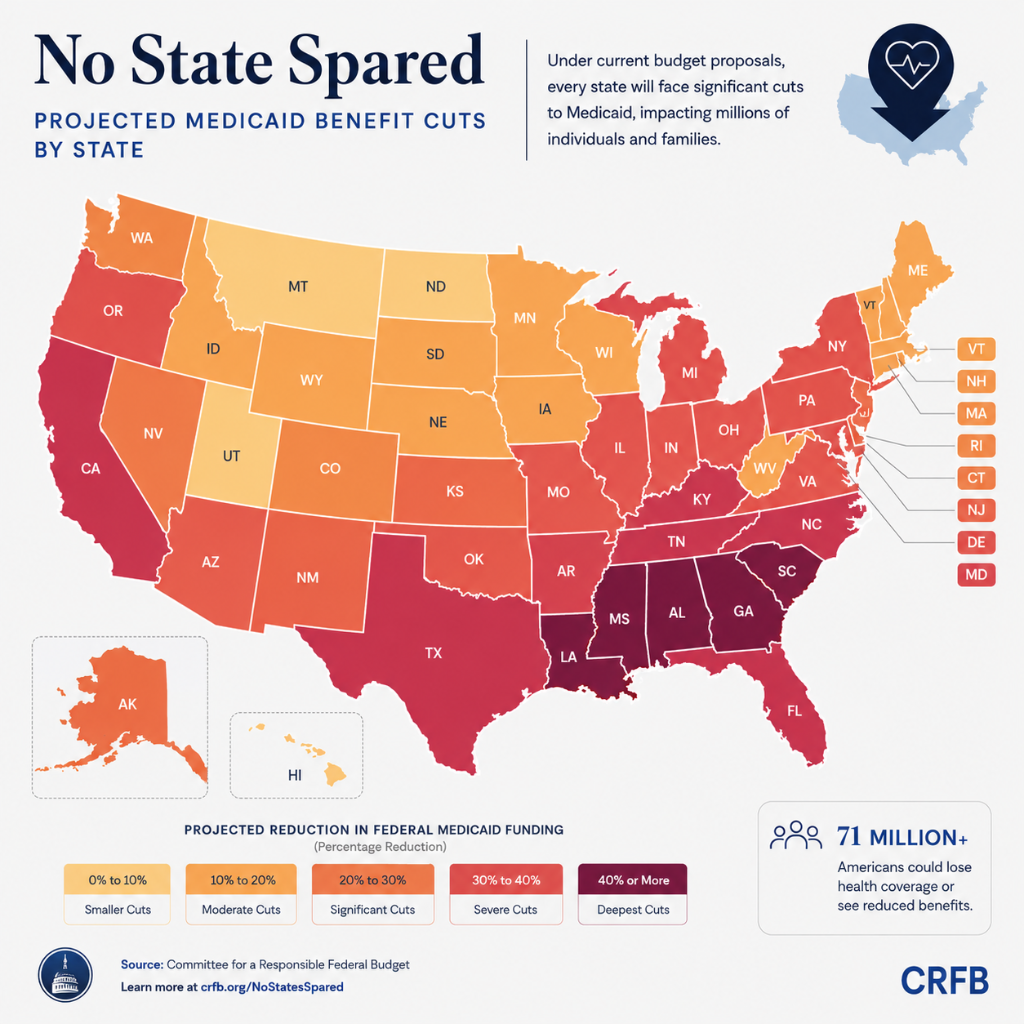

“No state would be spared from the potentially devastating effects of insolvency,” Committee for a Responsible Federal Budget, June 2026

Which States Face the Biggest Cuts? Your Complete State-by-State Guide

Here is where things get very personal, because the cuts are not the same in every state.

A June 2026 report from the Committee for a Responsible Federal Budget (CRFB) mapped out exactly what a 24% cut would mean for retirees in every single state. The results are striking.

In 29 states, the average monthly cut would be more than $500. The states facing the largest dollar cuts tend to be the ones where retirees currently receive higher average benefits, because a 24% cut of a bigger number means a bigger loss.

Top 10 States: Average Monthly Benefit Cut

| Rank | State | Avg Monthly Cut | % of Population Affected |

| 1 | Connecticut | $556 | 17.9% |

| 2 | New Jersey | $554 | 16.3% |

| 3 | New Hampshire | $553 | 21.0% |

| 4 | Delaware | $549 | 21.1% |

| 5 | Maryland | $541 | 15.6% |

| 6 | Washington | $531 | 16.7% |

| 7 | Minnesota | $530 | 17.7% |

| 8 | Massachusetts | $527 | 16.4% |

| 9 | Michigan | $523 | 19.8% |

| 10 | Utah | $523 | 12.1% |

| – | National Average | $500 | 17.7% |

Source: CRFB & Social Security Administration, June 2026

But it is not just about the dollar amount. It is also about how many people in each state depend on this money.

In Maine, a staggering 22.9% of the entire state population would be directly hit by the cuts. In West Virginia, it is 22.4%. In Vermont, 22.0%. In those states, about one out of every four or five folks walking down the street needs to worry about this.

When you look at how much it’ll cost each state, though, things get scary. The loss of benefits will top 1% of the GDP for 40 states. It hits places like West Virginia, Mississippi, and Vermont especially hard – around 1.8% to 1.9% of their GDP.

Benefits from retirees don’t just pad pockets; they keep local economies running. They support businesses and pay local taxes too. If their income falls, those economies really take a dive.

Who Are the 63 Million People Directly at Risk?

When you hear “63 million Americans,” it can feel like just a big number. But let’s think about who those people actually are.

That 63 million includes:

- 54 million retired workers who paid into Social Security their whole working lives and now rely on it in retirement

- 9 million survivors and dependents; this includes widows, widowers, and children of workers who have passed away

That is roughly 1 in every 5 Americans who would wake up one day in 2032 to find their monthly income suddenly and significantly reduced.

And a lot of these people have very little to fall back on.

A 2025 survey by the Senior Citizens League, a nonprofit group that tracks retirement issues, found that:

- 73% of retirees depend on Social Security for more than half of their total income

- 39% of retirees rely on Social Security for their entire income

Let that sink in for a moment. Nearly 4 out of 10 retirees have nothing else. No pension. No big investment account. No part-time job. Just their monthly Social Security check.

For those people, a 24% cut is not a financial inconvenience. It is the difference between a dignified retirement and genuine hardship.

Will Social Security Completely Stop? Let’s Clear Up the Confusion

This is the question a lot of people are silently asking. And the answer is: No. Social Security will not completely stop.

This is an important thing to understand. When people hear the word “insolvency,” they often picture Social Security just shutting off overnight. That is not what happens.

Even after the trust fund runs dry, workers across the country will still be paying payroll taxes every single month. That money still flows into the system. The program stays alive. The problem is that those incoming taxes will only cover 76 to 77% of the benefits owed.

By law, Social Security cannot pay out more than it takes in once the trust fund is gone. So instead of full benefits, retirees would automatically receive reduced benefits, the amount the program can actually afford to pay.

Your check still arrives. It is just noticeably smaller.

Here is why this distinction matters: some people hear “Social Security won’t collapse” and think there is nothing to worry about. But a 24% reduction in income for someone living on $1,500 a month is a very real and very painful problem, even if the program technically continues.

What Can Be Done to Fix This Before 2032?

Real Solutions to Prevent Social Security Benefit Cuts 2032

Here is some genuinely good news: this problem is fixable. It is not easy. It requires hard decisions and political will. But it is absolutely solvable, and there are real, concrete options on the table.

Option 1: Remove or raise the payroll tax income cap

Right now, Social Security payroll taxes are only collected on earnings up to $184,500 per year. If you earn more than that, the extra income is not taxed for Social Security purposes at all. Many policy experts argue that eliminating or significantly raising this cap would bring in far more revenue and could close a large portion of the funding gap on its own.

Option 2: Gradually raise the retirement age.

When Social Security began, folks didn’t live as long. Now, people commonly suggest bumping up the full retirement age since more live past eighty and ninety. Raising it bit by bit cuts how much the system pays out overall. So, it’s an adjustment to keep up with increased lifespans.

Option 3: Restructure how benefits are calculated

Some proposals suggest adjusting the benefit formula, especially for higher-income retirees who need it less, while keeping full protections in place for lower-income seniors who depend on it most.

Option 4: Act now, not later

This might be the most crucial point. Each year we don’t act makes the problem harder and more expensive to solve. If Congress steps in within the next year or two, they can use fairly modest changes to restore solvency. If they wait until 2031, the required changes become far more drastic, and far more painful for everyone.

The CRFB report makes this very clear: policymakers need to act quickly. With the insolvency date now projected during the terms of the next elected Senators and President, this is very much a current political issue, not a distant one.

What Should You Do Right Now? Practical Steps for Retirees and Near-Retirees

If you are already retired, or planning to retire in the next decade, here are five practical things you can do today. Not tomorrow. Today.

Step 1: Check your Social Security statement Online

Go to SSA.gov and log into your personal account. You can see your estimated monthly benefit at different retirement ages. This is your starting point. Know your number.

Step 2: Run a 24% cut scenario

Take your current or projected monthly benefit and multiply it by 0.76. That is what you would receive if the cut happened today. Can you cover your essential monthly expenses on that amount? If yes, great. If not, that is important information to act on now.

Step 3: Build or strengthen other income sources

Even small steps help. A part-time job, a small savings cushion, a modest investment, or a pension makes a real difference. Diversifying your retirement income means you are less exposed if Social Security gets cut.

Step 4: Watch the annual Trustees Report

The Social Security Administration releases an updated Trustees Report every year. The 2026 report is expected very soon. It will have the most current projections. Staying informed is one of the most powerful things you can do.

Step 5: Talk to your family about this

A lot of families have not had this conversation yet. If your parents or grandparents rely heavily on Social Security, a 24% cut in their income could directly affect your family too. This is worth talking about now, calmly and openly, so everyone can plan.

The Bottom Line

Let’s bring this all together.

The Social Security retirement trust fund is on track to run out of money by the end of 2032. When that happens, the law automatically cuts benefits by around 24%, which works out to roughly $500 less per month for the average retiree nationwide.

This is not a rumour. It is backed by official government projections and confirmed by independent fiscal policy research. Every single state in the country will be affected. No retiree, no community, no zip code is immune.

The good news is that the Social Security benefit cuts 2032 scenario is not inevitable. Real solutions exist. Policymakers have the tools to fix this, if they are willing to use them in time.

And on a personal level, knowing about this now, before it happens, gives you something incredibly valuable: time to prepare.

Review your finances. Check your statement. Have the family conversation. And stay informed as things develop over the next few years.

Because the earlier you understand what is coming, the better your chance of protecting yourself from it.

Related Reading

When Is Your Social Security Check Coming in June 2026?

Payment dates vary by birthday. Find your exact Wednesday, and what to do if your check is late.

Data & Sources Used in This Blog

| Source | What It Covers |

| CRFB.org: No State Spared Report (June 2026) | State-by-state benefit cut data, GDP impact, population affected |

| SSA.gov: 2025 Annual Trustees Report | Official insolvency projections and benefit levels |

| CBS News MoneyWatch (June 2026) | Reporting on the CRFB findings and state-level impact |

| BLS.gov: 2024 Consumer Expenditure Survey | Average retiree household spending on food |

| Senior Citizens League, 2025 Survey | Data on retiree dependence on Social Security income |

| Bureau of Economic Analysis, State GDP Data | State GDP figures used for economic impact calculations |

Disclaimer

This blog is for general informational purposes only. It does not constitute financial or legal advice. Always consult a qualified financial advisor for personal retirement planning guidance.