One mistake regarding your claiming period may silently eat away at hundreds of dollars from your monthly income for the rest of your life. This all depends on your knowledge about your Social Security Full Retirement Age.

This is no exaggeration. It is just how the math works.

Millions of Americans claim Social Security at 62 because they can. Not because they should. Some lose up to 30% of their monthly benefit permanently. Others wait too long and miss the income they genuinely need. This guide cuts through the confusion.

What Is Social Security Full Retirement Age?

Quick Answer

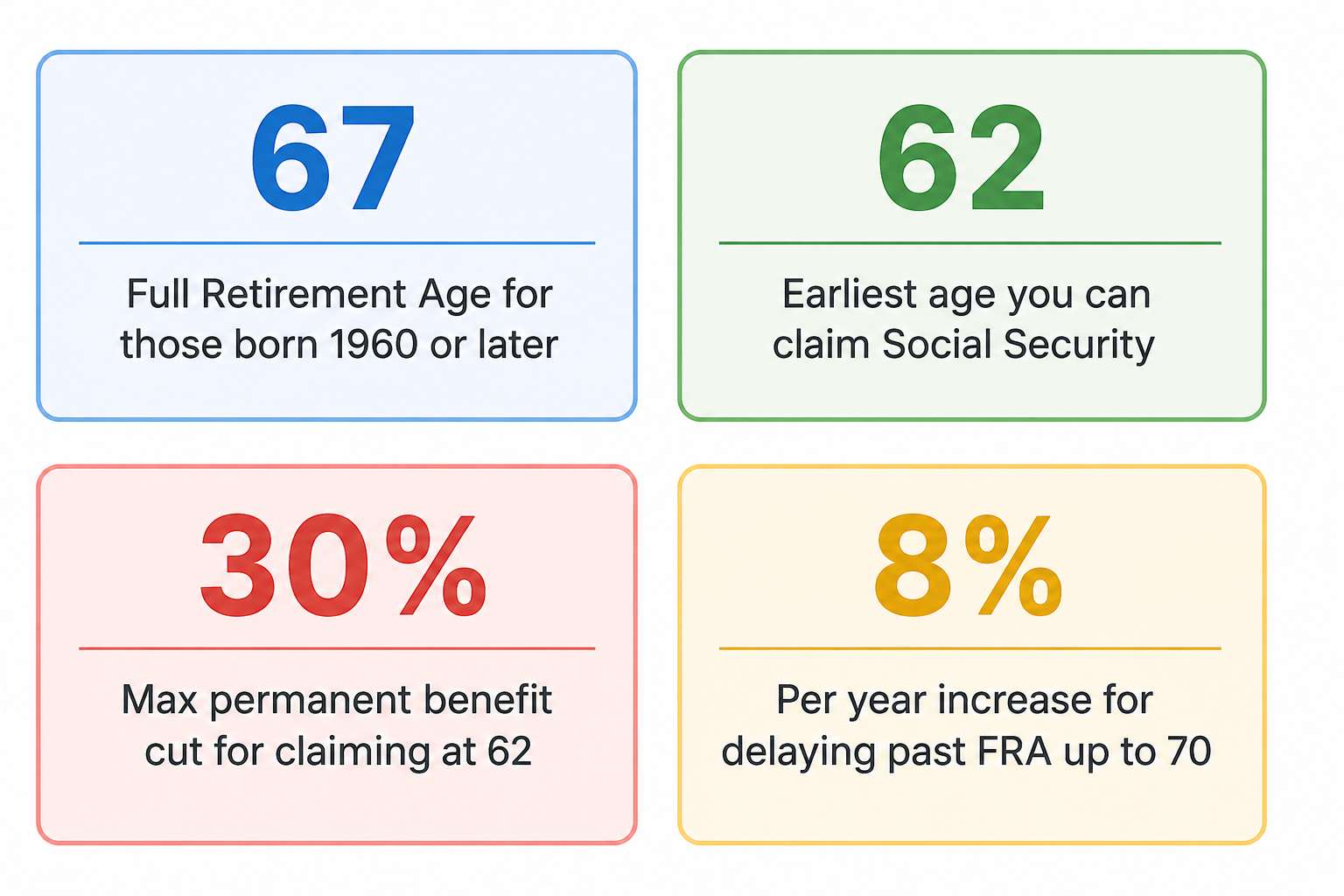

The Social Security Full Retirement Age (FRA) is the point when you get 100% of your benefits. Your FRA will vary from age 65 to 67 based on your birth date. Claiming before your FRA permanently lowers your benefit by up to 30%. Claiming after your FRA increases your benefit by 8% each year until age 70.

Your full retirement age, called FRA, is the government’s official benchmark for your retirement benefit. It is the age where you collect every dollar you earned through decades of payroll taxes. Not more, not less.

To anyone who is reading this today in 2026, 67 is that age. However, it was not always 67. It used to be 65 for many years before that. Congress decided to change it in 1983 due to longer life expectancies.

The shift happened gradually. If you were born in 1960 or later, your FRA is 67, full stop. The FRA for individuals born after 1960 is 67 only. If you were born between 1938 and 1959, then your FRA will range between 65 and 67.

How Is Full Retirement Age Determined?

The Social Security Administration sets your FRA based purely on your birth year. Your income, your work history, your health- none of that changes your FRA. Only when you were born does.

Two coworkers retiring the same year could have different full retirement ages if they were born in different years. This surprises a lot of people, and it is why checking your own FRA at SSA.gov matters more than asking a friend or neighbour.

The calculation is built into a chart. Once you know your birth year, your FRA is fixed. Here is the complete picture.

What Is the Full Retirement Age by Birth Year?

Social Security’s Full Retirement Age for anyone born after 1960 is 67; it is not going to change any time soon. The confusion starts with the transition period from 1955 to 1959.

| Birth Year | Full Retirement Age | Months Past 65 |

| 1937 or earlier | 65 | 0 months |

| 1938 | 65 and 2 months | +2 months |

| 1939 | 65 and 4 months | +4 months |

| 1940 | 65 and 6 months | +6 months |

| 1941 | 65 and 8 months | +8 months |

| 1942 | 65 and 10 months | +10 months |

| 1943–1954 | 66 | +12 months |

| 1955 | 66 and 2 months | +14 months |

| 1956 | 66 and 4 months | +16 months |

| 1957 | 66 and 6 months | +18 months |

| 1958 | 66 and 8 months | +20 months |

| 1959 | 66 and 10 months | +22 months |

| 1960 or later | 67 | +24 months |

Source: Social Security Administration, SSA.gov

If you were born in 1957, your FRA is 66 and 6 months, not 66, not 67. That six-month difference changes exactly when your full benefit kicks in. Six months may sound small. On a $1,800 monthly benefit, it is $10,800 in lost income if you get the date wrong.

Can You Claim Social Security Before Full Retirement Age?

Quick Answer

Yes. You can claim Social Security as early as age 62. But your monthly benefit is permanently reduced by up to 30% if you claim five years before your FRA of 67. The reduction does not reverse once you reach full retirement age; it stays for life.

The earliest claiming age is 62. It is historically one of the most common ages Americans start collecting, partly because they need the income, and partly because many do not realise the reduction is permanent.

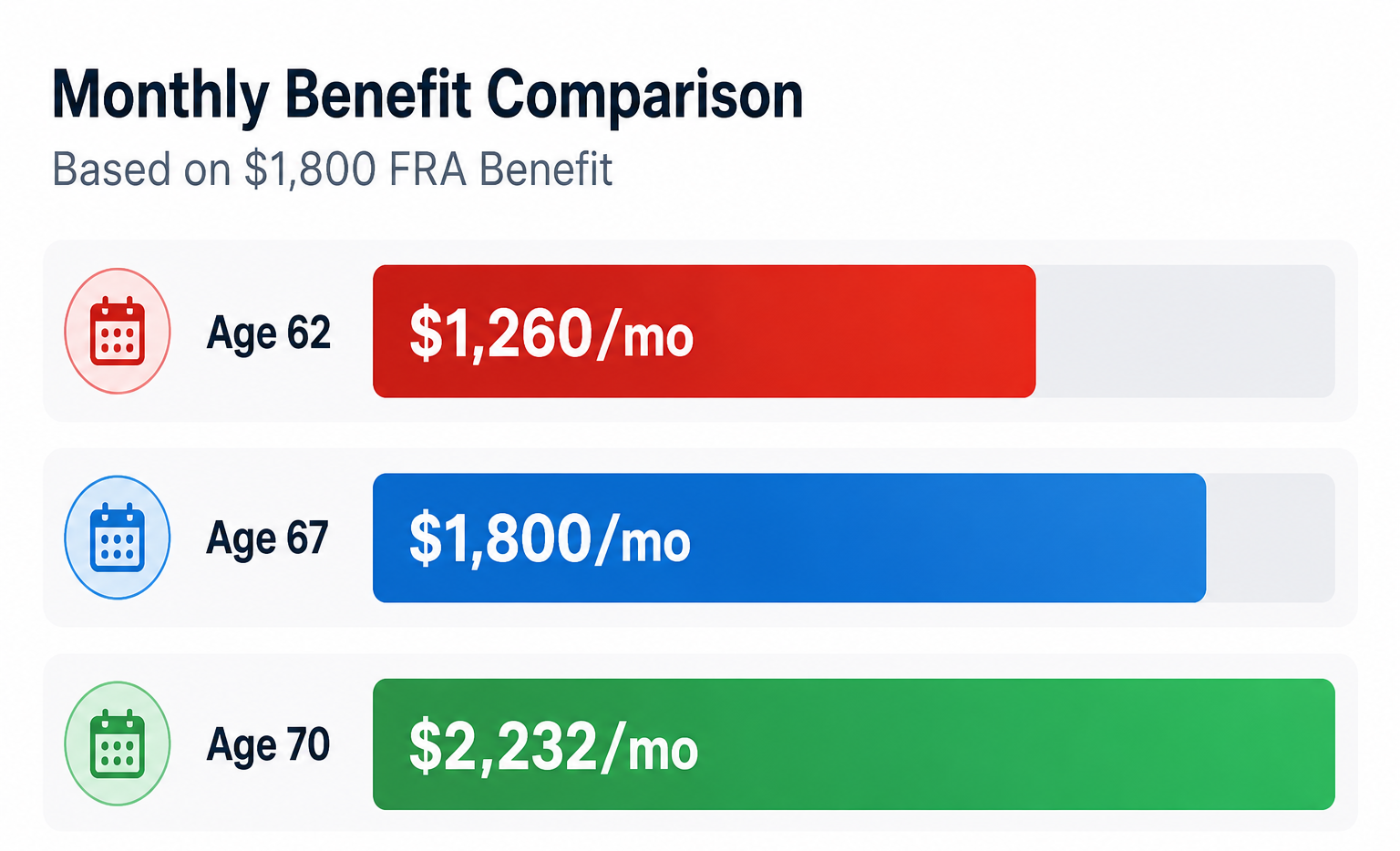

Monthly Benefit Comparison, Based on $1,800 FRA Benefit

| Claiming Age | Reduction from Full Benefit | Monthly Benefit (on $1,800 FRA) |

| 62 | Up to 30% reduction | ~$1,260/month |

| 63 | ~25% reduction | ~$1,350/month |

| 64 | ~20% reduction | ~$1,440/month |

| 65 | ~13.3% reduction | ~$1,560/month |

| 66 | ~6.7% reduction | ~$1,680/month |

| 67 (FRA) | No reduction | $1,800/month |

Source: SSA.gov, Retirement Planner

What Happens If You Delay Benefits Beyond Full Retirement Age?

Quick Answer

The consequences of delaying your Social Security benefits after your full retirement age would be an increase in your monthly payments due to the credit rate. Waiting from 67 to 70 increases your monthly benefit by approximately 24%. No additional credits apply after age 70.

Every year you delay past your FRA, the government adds 8% to your monthly benefit. Three years of delay, 67 to 70, adds 24% to your base benefit. On a $1,800 monthly benefit, that is an extra $432 every single month. For the rest of your life.

| Claiming Age | Monthly Benefit | Annual Benefit | After 20 Years Total |

| 62 | ~$1,260 | ~$15,120 | ~$302,400 |

| 67 (FRA) | $1,800 | $21,600 | $432,000 |

| 70 | ~$2,232 | ~$26,784 | ~$535,680 |

Based on $1,800 FRA benefit example. Source: SSA.gov benefit calculation methodology

The gap over 20 years between claiming at 62 versus 70 is over $233,000. That does not mean everyone should wait until 70 , but it means the decision deserves serious thought.

What Is the Earnings Limit Before Full Retirement Age?

Quick Answer

In 2026, if you claim Social Security before your full retirement age and still work, you can earn up to $22,320 per year without penalty. Above that, SSA temporarily withholds $1 for every $2 you earn over the limit. The earnings limit disappears completely once you reach FRA.

This catches a lot of people off guard. They claim at 62, keep working part-time, and then get surprised when their Social Security payments slow down or stop temporarily.

| Situation | 2026 Earnings Limit | Penalty Above Limit |

| Under FRA, full year | $22,320/year | $1 withheld per $2 over limit |

| Year you reach FRA | $59,520/year | $1 withheld per $3 over limit |

| At or past FRA | No limit | No penalty |

Source: SSA.gov, Earnings Test

Good news: The withheld money is not lost. Once you reach FRA, the SSA recalculates your benefit and gradually pays back what was held. But the cash flow gap during those years can be a real problem if you were counting on that income.

Social Security Benefits at 62 vs 67 vs 70, Who Should Do What?

Claim Early (Age 62–65) If…

- Your health is poor, or life expectancy is shorter

- You have no other income source

- You need cash flow now to cover essential bills

- Your spouse has a higher benefit and will delay

Delay to 67–70 If…

- You are in good health and your family lives long

- You have other income to cover the gap years

- You want the largest possible monthly check

- You are the higher earner in a married household

The break-even point for most people sits around age 80 to 82. If you live past that, waiting pays off financially. Family health history gives you a reasonable guide, though no one can know for certain.

📅 Know Your June 2026 Payment Date

Once you pick your claiming age, the next question is: when does the money actually arrive? Your payment date in June 2026 depends on your birthday — not on when you filed.

What Mistakes Should You Avoid When Claiming Social Security?

Claiming Without Knowing Your Social Security Full Retirement Age

This is the single most common and most costly mistake. People assume FRA is 65 because that used to be the standard. They claim at 65, and take a permanent benefit reduction they never planned for.

| Mistake | What It Costs You |

| Claiming at 62 without understanding the reduction | Up to 30% permanent monthly cut, forever |

| Not switching to electronic payments before the 2026 deadline | Risk of payment interruption – Social Security Electronic Payments Mandate 2026 see the full mandate guide |

| Not checking earnings record for errors | Missing years quietly reduce your benefit base |

| Ignoring spousal benefit strategy | Household misses thousands in combined lifetime income |

| Forgetting the 2032 insolvency risk | 24% automatic cut compounds on top of early-claiming cut |

| Not reviewing statement annually | Errors go uncaught and reduce your benefit permanently |

Important: A 24% automatic benefit cut is projected by the end of 2032 if the Social Security trust fund runs dry. Read our full breakdown guide on Social Security Benefit Cuts 2032: No State Will Be Spared before finalising any claiming decision. A large base benefit absorbs that cut far better than a reduced early-claiming benefit does.

How Can You Maximise Your Social Security Benefits?

Check your earnings record every year. Errors are more common than people think: missing years, wrong amounts, employer mistakes. Each error quietly reduces your benefit. Now read the full breakdown of our guide on How to Check Your Social Security Statement Online, A Step-by-Step Guide, which walks you through it in under 10 minutes at SSA.gov.

Coordinate with your spouse. If one of you earned significantly more, it usually makes sense for the higher earner to delay as long as possible. The lower earner can claim earlier. This strategy often produces the highest combined lifetime income for the household.

The Bottom Line

Retirement can last 25 or 30 years. The monthly benefit you lock in on your first claiming day follows you through all of it, every rent payment, every grocery run, every prescription.

Understanding your Social Security Full Retirement Age is the starting point for every other retirement income decision you make. Claim too early without knowing the cost, and you carry that reduction forever. Wait without a plan, and you may miss income you genuinely needed.

Know your FRA. Check your statement at SSA.gov. Understand the 2032 risk. Then make your decision from clarity, not guesswork. The goal is a retirement that holds up, month after month, for as long as you live.

Disclaimer

This blog is for general informational purposes only. It does not constitute financial or legal advice. Always consult a qualified financial advisor for personal retirement planning guidance.